What is a 509(a)(2) Public Charity and How is It Different from the Rest?

501c3 nonprofits must pass two tests with the Internal Revenue Service (IRS) to become a 509a2 organization. These tests measure where the nonprofit receives most of its funding and the organization’s sources of support. In this article, we discuss how 509a2 organizations are different from other nonprofits and how it can affect fundraising.

There are 27 different types of 501(c) nonprofit organizations defined by the Internal Revenue Service (IRS) that are exempt from federal income taxes. One of those categorizations is a 501(c)(3). Nonprofit religious organizations, charities, and educational facilities are just a few of the organizations that fall under this category. Within this category, the IRS has further split these organizations into five different groups.

This article will define 509(a)(2) organizations and how they are different from other nonprofits. It will also explain why a nonprofit should understand the difference between these organizations and how it may affect your fundraising.

What is a 509(a)(2) Public Charity?

A nonprofit must apply with the IRS to become a 509(a)(2) organization. A 509(a)(2) organization is primarily supported through income earned from performing its tax-exempt purpose. This income is often referred to as “mission-related income.” An example of this type of organization is a museum or zoo that receives most of its funding through admission fees.

509(a)(2) Public Support Test

Organizations that apply to become a 509(a)(2) organization must pass two tests by the IRS. Those tests consider where your organization is receiving the majority of its funding. The tests measure the organization’s sources of support over a five-year period, so if an organization has higher investment returns in one year, it does not mean it will automatically be categorized as a private foundation.

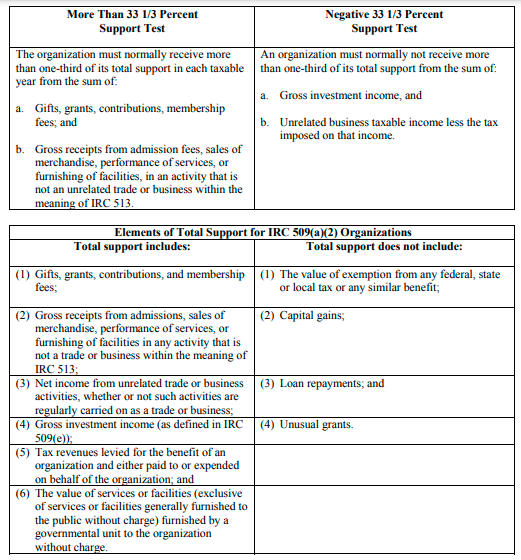

1. Positive 33.33% support test

509(a)(2) public charities must receive more than 33.33% of their income from:

Gifts, grants, contributions, and membership fees

Gross receipts from admission fees, sales of merchandise, the performance of services, or furnishing of facilities

2. Negative 33.33% support test

To qualify as a 509(a)(2) organization, an organization must receive less than 33.33% of its support from gross investment income and net unrelated business income.

Which Nonprofits are Considered 509(a)(2) Public Charities

An excellent example of a 509(a)(2) public charity is a museum or zoo. These organizations receive most of their revenue from membership and admission fees. Additional funds from gift shops and major donors still fall under public support.

Other organizations that may qualify as public charities under 509(a)(2) are nonprofit organizations that offer paid healthcare services. Nonprofit therapist offices offering these services to the public will fall under 509(a)(2) because a majority of their revenue may come from a combination of donations, grants, and payments for services provided.

How is a 509(a)(2) Different from Other 501(c)(3) Charities?

1. A 501(c)(3) charitable organization defined

The IRS provides tax-exempt status to all 501(c)(3) organizations. To receive this exemption, an organization must apply with the IRS unless they are a church. Organizations that provide the following services can qualify for 501(c)(3) tax exemptions:

Religious

Charitable

Scientific

Testing for public safety

Educational

Fostering of national or international amateur sports

Prevention of cruelty to animals and children

2. The main difference between 501(c)(3) and 509(a)(2)

Private foundations, 509(a)(1), 509(a)(2), and 509(a)(3) public charities, as well as private operating foundations, all fall under the 501(c)(3) tax-exempt status.

A 501(c)(3) organization is presumed to be a private foundation until they prove they are a public charity. Once they have proved they are a public charity, a nonprofit will then be distinguished as a 509(a)(1), 509(a)(2), or 509(a)(3) public charity. This is important because donations to a private foundation and public charity are taxed differently. Your supporters will want to know the difference.

Donors who give to a public charity can deduct up to 60% of their adjusted gross income (AGI) from their annual taxes. A donation to a private foundation may be limited to 30% of their AGI.

3. Private foundations vs. public charities

A single individual or business generally creates private foundations. A private foundation must be built to meet the charitable priorities of a 501(c)(3) organization. The founder will often donate a significant amount to invest and create income and thus retain a significant pull over the organization’s activities. Private foundations will provide grants to organizations that have programs that meet the foundation’s goals.

Public charities carry out specific charitable activities that qualify the organization for tax-exempt status as a 501(c)(3) organization. These public charities must solicit donations from the public.

The main difference between the two is how they collect funds. Private foundations can receive a majority of their income from investments. A public charity must receive mostly public support over five years.

What Other Income Limits Are There for a 509(a)(2) Charity?

There are limitations to what income qualifies as public support. A 509(a)(2) organization will need to pay close attention to where each source of revenue comes from. The IRS has limited specific income from activities that are not unrelated to trades or businesses to $5,000 or 1% of the organization’s total annual support. These limits apply year to year, not cumulatively. The goal is to make sure public support is really public.

The following are examples of donors and gifts that are subject to this rule:

1. Disqualified persons

A disqualified person is defined as “any person who was in a position to exercise substantial influence over the affairs of the applicable tax-exempt organization…it is not necessary that the person actually exercise substantial influence, only that the person can be in a position to do so.” All donations from disqualified persons are entirely excluded from public support when calculating income received.

The following are examples of disqualified persons:

Major donors – any person who contributed more than $5,000 or 2% of the organization’s total contributions since its start

Officers, directors, trustees, and individuals with similar powers or responsibilities

Owners of a business that is a major donor

Family members of disqualified persons

Corporations owned by disqualified persons

Partnerships owned by disqualified persons

Entities owned by disqualified persons

2. Grants

Grants that fund the organization’s programs to address the nonprofit’s tax-exempt purpose are different from gross receipts and can count in full as public support. Also, those that are provided to serve the direct and intermediate needs of the funder will qualify as gross receipts and are limited to the $5,000 or 1% rule.

3. Membership dues

If an organization’s memberships program exists only to provide admissions, merchandise, services, or the use of facilities to those who otherwise have no consideration for the nonprofit’s tax-exempt purpose, their membership fees are classified as gross receipts. These membership fees are subject to the $5,000 or 1% rule.

4. Thrift shops

Gross receipts from thrift stores, convenience shops, and businesses operated by charitable organizations where substantially all work is performed by volunteers are subject to the $5,000 or 1% rule.

5. Governmental unit’s bureau or agency

Governing bodies whose purpose is policymaking or administration will fall under the $5,000 or 1% rule. Income received from these bureaus or agencies is seen as gross receipts and is, therefore, limited.

Conclusion

A 509(a)(2) public charity will need to find support from various places, including grants, donations, and payments for services rendered. These organizations depend on the public’s help for their survival. On the other hand, a private foundation can survive on investment income and may be an individual or family’s tool to address a problem. Nonprofits must understand the difference between these two organizations when collecting donations from specific sources or addressing tax deduction questions from their donors.

Our Donorbox blog provides tips, resources, and best practices for nonprofits. We also have dedicated articles for starting a nonprofit in different states in the US, including Texas, Minnesota, Oregon, Arizona, Illinois, and more.

Our affordable online donation processing system offers nonprofits the chance to collect more donations and reach more donors online. If you’re looking for powerful features for your nonprofit, such as an online donation form, donation page, text-to-give, a peer-to-peer fundraising solution, crowdfunding, event ticketing, memberships, and more, check out the Donorbox website.

Frequently Asked Questions (FAQs)

We’ll answer a couple of questions on the 509(a)(2) public charity and other related charity types.

1. How can a new organization become a public charity?

Nonprofits that are just starting out do not have five years of donation history, so deciding where they receive most donations from is just a guess. The IRS has provided a way for new organizations to meet the support tests required for a 509(a)(2) organization.

If the nonprofit’s organizational structure, programs, and fundraising method will attract more public support, the organization can reasonably expect to meet the IRS’s expectation of a public charity. The IRS can determine this when nonprofits register for tax-exempt status.

According to the Deficit Reduction Act of 1984, if the nonprofit can reasonably expect to meet the support tests after five years, the IRS will issue a determination letter. If the organization does not meet the standards after five years, it will automatically qualify as a private foundation.

2. What are 509(a)(1), 509(a)(3), and 509(a)(4) organizations?

A 509(a)(1) is the most common nonprofit. These public charities receive at least 1/3 of their income from the public through gifts, grants, contributions, and membership fees. Examples of this type of public charity are churches, schools, hospitals, and other similar organizations.

A 509(a)(3) is a supporting organization and is subordinate to another 501(c)(3) nonprofit. While there are private foundations that support public 501(c)(3) nonprofits, a 509(a)(3) must have a relationship that allows supervision over the supporting organization’s activities.

A 509(a)(4) organization is a public safety charity. This type of organization is rare but does qualify as a public charity.

Kristine Ensor is a freelance writer with over a decade of experience working with local and international nonprofits. As a nonprofit professional she has specialized in fundraising, marketing, event planning, volunteer management, and board development.